Even before the coronavirus sprang upon an unprepared China the credit cycle was tipping the world into recession.The coronavirus makes an existing situation immeasurably worse,shutting down China and disrupting global supply chains to the point where large swathes of global production simply cease.

甚至在这种冠状病毒突然袭击毫无准备的中国之前,信贷周期就已经使世界陷入衰退。这种冠状病毒使得目前的形势恶化到无法估量的地步,它关闭了中国,扰乱了全球供应链,以至于大量的全球生产完全停止。

The crisis is likely to be a wake-up call for complacent investors,who are content to buy benchmark bonds issued by bankrupt governments at wildly excessive prices.A recession turned by the coronavirus into a fathomless slump will lead to a synchronised explosion of debt issuance for which there are no genuine buyers and can only be monetised.

这场危机可能会为自满的投资者敲响警钟,他们满足于以极高的价格购买破产政府发行的基准债券。冠状病毒引发的衰退转变为深不可测的衰退,将导致同步爆发的债务发行,而这些债务没有真正的买家,只能货币化。

The adjustment to reality will be catastrophic for government finances,and their currencies.This article explains why the collapse in overpriced financial assets and fiat currencies is likely to be rapid,perhaps giving ordinary people in some jurisdictions an early prospect of a return to gold and silver as circulating money.

面对现实的调整将给政府财政及其货币带来灾难性后果。这篇文章解释了为什么定价过高的金融资产和法定货币可能会迅速崩溃,或许会让某些地区的普通民众早日看到回归金银作为流通货币的前景。

Introduction

引言

My last article suggested that both financial assets and currencies would collapse together.the basis of this supposition is twofold:first,central bank policies are binding together the rise in financial assets with the maintenance of value in fiat currencies.Therefore,if one falls,they both fall.And secondly there is historical precedence for this when one examines The Mississippi bubble 300 years ago.

我的上一篇文章指出,金融资产和货币将同时崩溃。这种假设的基础有两个方面:第一,中央银行的政策将金融资产的增加与法定货币的保值联系在一起。因此,如果一个人摔倒了,他们两个都会摔倒。其次,当我们回顾300年前的密西西比泡沫时,我们会发现历史上的先例。

The timing for such a collapse appears to be imminent.Every day,more and more data confirm that the global economy is sliding into recession.So far,people have been ignoring this important development,but now that it is becoming hard to ignore,no doubt the coronavirus will be blamed.This is a mistake because the factors leading to a slump,principally the end of the expansionary credit cycle combining with trade protectionism against Chinese imports by President Trump,echo developments leading up to the Wall Street crash in October 1929.If that point is accepted,then clearly the world could be on the edge of a very deep slump exacerbated but not caused by the virus.

这种崩溃的时机似乎很快就会到来。每天都有越来越多的数据证实,全球经济正滑向衰退。到目前为止,人们一直忽视这个重要的发展,但是现在它变得越来越难以忽视,毫无疑问冠状病毒将受到指责。这是一个错误,因为导致衰退的因素,主要是扩张性信贷周期的结束,加上特朗普总统针对中国进口的贸易保护主义,呼应了导致1929年10月华尔街崩盘的事态发展。如果这一点被接受,那么很明显,世界可能处于非常严重的衰退的边缘,这种衰退会加剧,但不是由病毒引起的。

The coronavirus has all but closed down China's economy.It threatens to become a pandemic with serious consequences for all other national economies and their fiat currencies.

这种冠状病毒几乎使中国经济陷入瘫痪。它有可能成为一种流行病,对所有其它国家的经济及其法定货币造成严重后果。

The central issue flowing from the upcoming monetary crisis centres on the rating of government debt.Almost all welfare-driven states are in debt traps.They think price inflation is under control,because their colleagues in the statistics departments tell them so,allowing them to continue to run increasing budget deficits with apparent impunity.Central banks do not realise that very soon they will be the only buyers of their governments'debt which they will pay for with newly minted money.The irony of repeating the mistakes of Germany's Reichsbank in 1918-23 will be completely lost to them and the path of escalating failure will only encourage the pace of printing to be accelerated.

即将到来的货币危机的核心问题是对政府债务的评级。几乎所有以福利为导向的国家都陷入了债务陷阱。他们认为物价上涨已经得到控制,因为他们在统计部门的同事告诉他们这一点,这使得他们可以继续运行不断增加的预算赤字而明显不受惩罚。各国央行没有意识到,很快它们将成为本国政府债务的唯一买家,它们将用新发行的货币来偿还这些债务。具有讽刺意味的是,重复德国国家银行(Reichsbank)在1918年至1923年犯下的错误,这种错误将完全被他们遗忘,而不断升级的失败之路只会鼓励加快印刷速度。

The latest bombshell,coronavirus,is a trigger perhaps for the markets to regain control from the statist price riggers.This has to be the first step to fixing broken economies.The Panglossians in the ranks of the banking and investment communities will be rudely awakened to find themselves staring down the barrel of economic reality.Only then is there a chance that neo-Keynesian lies will be discarded by one and all,and a retreat towards sound money commence.

最新的重磅炸弹,冠状病毒,或许是市场从中央集权的价格敲诈者手中夺回控制权的触发器。这必须是修复破碎经济体的第一步。银行界和投资界的盲目乐观者将被粗暴地唤醒,发现自己正盯着经济现实的大桶。只有这样,新凯恩斯主义的谎言才有可能被所有人抛弃,开始向健全货币的退却。

There is unlikely to be much time.Even without the downhill kick of coronavirus a bear market in bonds could be a devastating event on its own in a period of less than a year.Inflation of fiat currencies and interest rate suppression have been the principal agents for ramping bond prices,which tells us that their collapse will undermine currencies as well,giving complacent investors a double hit.But what are we to measure a decline of fiat currencies against?Sound money of course,gold and silver,with other stores of value,such as bitcoin,favoured by tech-savvy millennials,who will be quick to observe and understand the debauchment of fiat money.And the sooner we throw out fiat currencies,the sooner we can revert to sound money,which is gold.

时间可能不多了。即使没有冠状病毒的走下坡路,在不到一年的时间里,债券市场的熊市本身也可能是毁灭性的事件。法定货币的通胀和利率的抑制一直是推高债券价格的主要因素,这告诉我们,这些货币的崩溃也会损害货币,给自满的投资者带来双重打击。但我们如何衡量法定货币兑美元汇率的下降呢?当然,稳健的货币是黄金和白银,还有其他价值储存,比如比特币,这种货币受到精通技术的千禧一代的青睐,他们会很快观察和理解法定货币的堕落。我们越早抛弃法定货币,我们就能越早恢复健全的货币——黄金。

Changing values for government bonds

改变政府债券的价值

We shall take as our primary example the US bond market,because fiat currency fans believe that other than individual time-values it is the risk-free investment yardstick.The ten-year US Treasury bond yields less than 1.6%,but its future pricing raises some serious issues.

我们将以美国债券市场为主要例子,因为法定货币爱好者认为,除了个人的时间价值外,法定货币市场是无风险的投资标准。十年期美国国债收益率不到1.6%,但其未来定价引发了一些严重问题。

Before addressing risk,we should note that time preference theory tells us that possession of cash is always worth more than its non-possession.The discount of that future value is not significant if you part with it to buy a ten-year UST with a view to trading it out in the next few days.But if you buy it with a view to holding it as an investment,then its discounted future value does become relevant.We cannot know what this time preference is,because it can only be realised in an unfettered market,not a market manipulated by the Fed's actions.But with history as our guide an annualised discounted value of about two per cent for a 10-year bond can be used as a rough guide.

在讨论风险之前,我们应该注意到时间偏好理论告诉我们,拥有现金总是比没有现金更有价值。如果你为了在接下来的几天里买一个10年期的 UST 而放弃它,那么这个未来价值的折扣并不重要。但是如果你购买它是为了将其作为一种投资,那么它的未来价值的折现就变得相关了。我们无法知道这一次的偏好是什么,因为它只能在一个不受约束的市场中实现,而不是一个受美联储行动操纵的市场。但以历史为参照,10年期债券折合成年率约为2%的贴现价值可以作为一个粗略的参考。

Figure 1,which is a long-term chart of the yield on this bond,appears to indicate there is a solid floor in the region of 1.4%represented by the horizontal line joining points at July 2012,July 2016 and August 2019.This floor is about half a per cent less than our estimated time preference value.

图1是这种债券收益率的长期图表,似乎表明在2012年7月、2016年7月和2019年8月的横向连线点所代表的1.4%区域有一个坚实的底部。这个下限比我们估计的时间偏好值低了大约0.5%。

With its yield currently 1.56%,there appears to be very little upside in the price,and we can understand why.And if we accept government estimates of CPI-U all items index rising at 2.5%(year to January)the yield should be closer to 4%and must therefore be heavily suppressed at current levels.

目前其收益率为1.56%,价格似乎没有什么上涨空间,我们可以理解其中的原因。如果我们接受政府对 CPI-U 所有项目指数上涨2.5%的估计,那么收益率应该接近4%,因此必须在当前水平上大力压制。

That is not all.While the general level of prices is an economic concept,it is not measurable;a fact which allows the Bureau of Labour Statistics,along with all other nations who use"standardised"CPIs to effectively goal-seek an official figure for its rate of change.Two independent analysts,Chapwood Index and Shadowstats confirm each other that a more realistic rate for monetary depreciation of the US dollar is not 2%,but about 10%annually.

这还不是全部。虽然一般价格水平是一个经济概念,但它是无法衡量的;这一事实使得劳工统计局和所有其他使用"标准化"消费物价指数的国家能够有效地实现目标——为其变化率寻求一个官方数字。查普伍德指数和 Shadowstats 两位独立分析师相互证实,更为现实的美元贬值率不是2%,而是每年10%左右。

But for the moment,investors believe the price inflation lie because they want to.When they begin to realise the official rate is pure fiction,then one would expect government bonds to reflect a far higher redemption yield.In other words,any upside in bond prices is strictly limited while the downside is substantial.As an illustration,a 10-year bond at the current yield would have to fall from par to$47.40 to yield a more realistic gross 10%to redemption.

但就目前而言,投资者认为,价格通胀之所以存在,是因为他们想这么做。当他们开始意识到官方利率纯属虚构时,人们就会认为政府债券的赎回收益率要高得多。换句话说,债券价格的任何上涨都受到严格限制,而下跌的幅度则是巨大的。举例来说,以当前收益率计算,10年期债券必须从面值降至47.40美元,才能获得更实际的10%的赎回总额。

Clearly,the US Treasury market is badly mispriced.To estimate the likelihood of the Fed losing control of bond pricing,we should also take into account the state of the US Government's finances,because we have not yet incorporated future currency debasement risks in our calculations.With a starting budget deficit in the current fiscal year estimated by the Congressional Budget Office at$1,027bn,a recession,let alone a slump,will make government finances considerably worse.For the years 2020-2022 the CBO expects real GDP to grow at an average 2%per annum.In the very near future,due to the coronavirus alone that is likely to be revised sharply downwards,if not by the CBO,but by market participants as further evidence of a looming slump becomes too hard to ignore.

显然,美国国债市场的定价严重错误。要估计美联储失去对债券定价控制的可能性,我们还应考虑美国政府的财政状况,因为我们尚未在计算中考虑到未来货币贬值的风险。美国国会预算办公室(Congressional Budget Office)估计,本财年的预算赤字将达到1.027万亿美元,因此,经济衰退(更不用说衰退)将使政府财政状况大幅恶化。国会预算办公室预计,2020-2022年,实际国内生产总值每年平均增长2%。在不久的将来,由于冠状病毒本身可能被大幅下调,如果不是由国会预算办公室,而是由市场参与者作为进一步的证据,即将出现的经济衰退变得难以忽视。

All we need to know for now is the revision of economic prospects will be significant,based on recent evidence of recessionary trends and the potential impact of the coronavirus.The current stage of the credit cycle indicates the banks are in the process of withdrawing circulating credit,hitting SMEs particularly hard.Unemployment will rise,along with bankruptcies.And this assumes little or nothing for the effect of coronavirus.

我们现在需要知道的是,根据经济衰退趋势和冠状病毒潜在影响的最新证据,经济前景的修正将是重大的。目前信贷周期的阶段表明,银行正在撤销流动信贷,对中小企业的打击尤为严重。随着破产,失业率将会上升。这对冠状病毒的作用假设很少或根本没有。

But even if coronavirus is contained to China and East Asia,US corporations'supply chains will cease to function,requiring both time and bank credit to relocate.Neither are available in the short term and in the current credit climate.And this is an election year,when any president's financial and economic prudence are at their lowest ebb and his administration is most inclined to throw money at any and all economic problems.

但是,即使冠状病毒被控制在中国和东亚,美国企业的供应链也将停止运作,需要时间和银行信贷来重新安置。在当前的信贷环境下,短期内两者都无法实现。今年是选举年,任何一位总统在财政和经济上的谨慎态度都处于最低潮,而他的政府最倾向于把钱投向任何和所有的经济问题。

Without a recession,other things being equal the CBO's forecasting assumptions and the effect on government debt outstanding might be taken to be credible by gullible investors.But expressed in the economist's jargon,not all else is equal and we can already see why these forecasts are going horribly wrong.The question then is what the effect on markets will be when these errors are realised and prices for financial assets are adjusted for reality.

如果没有经济衰退,在其它条件相同的情况下,美国国会预算办公室的预测假设和对未偿政府债务的影响,可能会被容易上当的投资者认为是可信的。但是用经济学家的术语来说,并不是所有其他因素都是相等的,我们已经可以看出为什么这些预测会出现严重的错误。接下来的问题是,当这些错误被发现,金融资产的价格根据实际情况进行调整时,市场将受到何种影响。

The adjustment will follow the current period of complacency.US Treasury bond prices have recently risen,partly on a safe-haven basis,but certainly with an enduring belief in the state's economic management.Equities are at or close to all-time highs on a relative value to bond yields argument,and an expectation that any recession will be shallow.Further monetary easing is expected to support the economy and maintaining the long-term prospect of a resumption to decent economic growth.Further monetary easing is seen to be bullish.

此次调整将遵循当前的自满时期。美国国债价格最近有所上涨,部分原因是出于避险的考虑,但肯定是因为人们对政府的经济管理抱有持久的信心。根据相对价值与债券收益率的关系,股市目前处于或接近历史高位,而且市场预期任何衰退都将是轻微的。预计进一步的货币宽松政策将支持经济,并保持经济恢复体面增长的长期前景。人们认为,进一步放松货币政策将是利好。

Concerns about the dollar are broadly absent.There is embedded in investor psychology Part One of Triffin's dilemma,that concludes otherwise irresponsible fiscal policies will allow the provider of the world's reserve currency to run deficits to increase its supply to foreigners,always hungry for scarce dollars,which they reinvest in US Treasuries.And if there is a recession,the argument goes,then there will always be a further flight to the safety of dollars and US Treasuries.

对美元的担忧基本上不存在。投资者心理已经成为特里芬两难困境的一部分。这一部分得出的结论是,否则,不负责任的财政政策将使这个全球储备货币的提供者出现赤字,从而增加对外国人的供应。外国人总是渴望稀缺的美元,他们将这些美元再投资。这种观点认为,如果经济出现衰退,那么投资者总会进一步转向安全的美元和美国国债。

Part Two of Triffin's dilemma ends in crisis,which broadly is what we now face.Investors are yet to take note.

特里芬困境的第二部分以危机告终,这也是我们现在面临的问题。投资者尚未注意到这一点。

Putting the effects of the coronavirus to one side for the moment,in their private capacity businessmen and their bankers are usually the first to see that economic optimism is misplaced.Businessmen are battling in deteriorating trading conditions,and bankers with their internal market intelligence and its impact on risk assessment.The authorities,particularly the Fed,who have made the mistake of believing in their own statistics,and of falling hook,line and sinker for Keynesian stimulation theories,will be next.

暂时把冠状病毒的影响放在一边,在他们的个人身份下,商人和他们的银行家通常是第一个看到经济乐观主义是错误的。商人们正在不断恶化的交易环境中苦苦挣扎,而银行家们则在利用他们的内部市场情报及其对风险评估的影响进行战斗。当局,尤其是美联储,错误地相信了自己的统计数据,错误地相信了凯恩斯主义的刺激理论。

One can envisage the setup:having seen from its own internal information the economy is not performing as hoped,the Fed decides to call in the management of the G-SIB banks to hear their concerns,gather intelligence and reassure them they are on the case.Afterwards,we can imagine the following conversation:

人们可以设想这样的局面:从美联储自身的内部信息来看,经济表现不如预期,美联储决定召集 G-SIB 银行的管理层,听取他们的担忧,收集情报,并向他们保证,他们正在处理此事。之后,我们可以想象下面的对话:

Banker A."Well,what did you make of that?"

银行家答:"那么,你是如何看待这个问题的?"

Banker B."The Fed must be worried to feel the need to reassure us.Things must be worse than we thought."

银行家 b。"美联储一定很担心,觉得有必要让我们放心。情况肯定比我们想象的更糟。"

Bankers A&B.(Thinking)I'll report back to my Board that the Fed is very worried,and we must urgently reduce our loan book before our competitors do.

我将向我的董事会报告,美联储非常担忧,我们必须在我们的竞争对手之前紧急减少我们的贷款。

It has happened before.None of this would occur in an economy which is based on sound money and free markets,only susceptible to one-off disasters,such as war and the coronavirus.Instead,the US economy is managed on the basis of maintaining the crumbling confidence of consumers and the uninterrupted provision to them of credit.After many years of being bailed out,economic actors have become fully dependent on confidence being maintained and have no alternative plan in the case of its failure.But failure is now becoming evident.

这种情况以前也发生过。在一个以健全的货币和自由市场为基础的经济体中,这一切都不会发生,只会受到战争和冠状病毒等一次性灾难的影响。相反,美国经济的管理是建立在维持日益崩溃的消费者信心和不间断地向他们提供信贷的基础之上的。经过多年的纾困之后,经济行为者已经完全依赖于信心的维持,如果信心失灵,他们别无选择。但是现在失败变得越来越明显。

The central question therefore devolves upon the future credit rating of the US Government.Assuming the Fed is losing control of the overall monetary situation and pricing returns to being set by markets,how do you rate a very large borrower with the following credit profile:

因此,中心问题转移到美国政府未来的信用评级上。假设美联储正在失去对整体货币形势和定价回报的控制,而由市场决定,那么对于一个信用状况如下的大型借款人,你如何给它评级:

No surplus of income over expenses since 2001.Current trend is for further deterioration with no end in sight.

自2001年以来没有收入超过支出的盈余。目前的趋势是进一步恶化,而且看不到尽头。

Net present value of future liabilities mandated by law is independently estimated(Kotlikoff)to be over$200 trillion.Current income(taxes etc.)of$3.6 trillion gives a ratio of income to future expense of well over 50 times.Tax income will almost certainly decline raising this ratio further.

法律规定的未来债务的净现值被独立估计超过200万亿美元。目前的收入(税收等)为3.6万亿美元,使得收入与未来支出的比率远远超过50倍。税收收入几乎肯定会下降,进一步提高这一比例。

Net interest cost at unrealistically low interest rates is 38%of last year's deficit.A more realistic interest rate could have an immediate and catastrophic effect on finances.

在不切实际的低利率下,净利息成本是去年赤字的38%。更为现实的利率可能会对金融产生立竿见影的灾难性影响。

Management seems unjustifiably optimistic that future revenue will pick up.

管理层似乎毫无道理地乐观地认为未来收入将会回升。

In the absence of a management that agrees to radically alter course,there can only be one answer:do not lend it any money and eliminate all existing exposure.When they wake up,this should,and therefore will be,the reality facing not just the banks but all holders of US Treasuries,including foreigners without sound reasons to be invested in them.

如果管理层不同意彻底改变方向,那么只有一个答案:不借钱给它,消除所有现有的风险敞口。当他们清醒过来时,不仅银行,而且所有美国国债持有者,包括没有充分理由投资美国国债的外国人,都应该(因此将会)面对这样的现实。

Consequently,the switch from the current state of suppressive control to realistic pricing of government debt will be both vicious and rapid.The only foreigners likely to delay selling existing US Government debt are some governments,either under the US Government's cosh,or not wishing to exacerbate the situation.With cross-border trade collapsing,others have no good reason to hold dollars and dollar-denominated debt,let alone extend their exposure.Furthermore,in recent years large hedge funds have made hay out of being short euros and yen and long dollars and US Treasury debt through fx swaps.Those trillion-dollar positions need to be unwound as well,which will put additional pressure on the dollar and the bond markets.

因此,从目前的抑制性控制转向现实的政府债务定价将是恶性和快速的。唯一可能推迟出售现有美国政府债券的外国人是一些政府,它们要么受到美国政府的怂恿,要么不希望恶化局势。随着跨境贸易崩溃,其它国家没有充分理由持有美元和美元计价债券,更不用说扩大它们的风险敞口了。此外,近年来,大型对冲基金通过外汇互换,从做空欧元、日元、多头美元和美国国债中大赚了一笔。这些万亿美元的头寸也需要平仓,这将给美元和债券市场带来额外压力。

At anything close to these yields,the only buyer will be the Fed,which,as well as new issuance will have to absorb foreign sales and those of distressed hedge funds.For these reasons the monetisation of debt will almost certainly have to be on a far larger scale than following the Lehman crisis.There is no price for government debt in these circumstances,because the higher the interest rate,the worse the numbers become.Nor will there be any value in the currency used to buy it,because if the government is effectively bust its unbacked currency will also be worthless.

在任何接近这些收益率的情况下,唯一的买家将是美联储,美联储以及新发行的债券将不得不吸收外国投资者和陷入困境的对冲基金的出售。出于这些原因,几乎可以肯定,债务货币化的规模将远远大于雷曼危机之后的规模。在这种情况下,政府债务是没有代价的,因为利率越高,数字就越糟糕。也不会有任何价值的货币用于购买它,因为如果政府实际上是破产,其无支持的货币也将是一文不值。

Other governments with substantial future welfare commitments are in a similar position.High debt to GDP ratios will become a debt trap on a combination of recession-fuelled budget deficits and realistic funding costs.In the EU and Japan,government funding costs have even further to travel from under the zero bound.

其他有着巨大未来福利承诺的政府也处于类似的境地。高债务与国内生产总值(GDP)的比率将成为一个债务陷阱,这是由衰退推动的预算赤字和现实的融资成本共同作用的结果。在欧盟和日本,政府的资金成本甚至比零下限还要高。

Meanwhile,there is an air of complacency with a general assumption that the next crisis will lead to yet lower rates,as has been the case with every credit crisis for the last forty years.But as Figure 1,the chart of the ten-year US Treasury above clearly showed,after a long decline in yields the world's reserve currency benchmark yield is now struggling to go any lower.Zero or even negative dollar rates imposed by the Fed cannot alter that fact.

与此同时,人们普遍自满地认为,下一场危机将导致利率进一步下降,过去40年来的每一次信贷危机都是如此。但正如图1所示,美国10年期国债的图表清楚地显示,在收益率长期下降之后,全球储备货币基准收益率现在正在努力走低。美联储实施的零甚至负美元利率不能改变这一事实。

This is important,because central banks have tried everything that they can think of to restore economic growth and have run out of ideas.Led by the Bank for International Settlements,they are now pleading with their governments to borrow more while rates are cheap in the hope that greater budget deficits will stop the world from sliding into recession.

这一点很重要,因为各国央行已经竭尽所能,试图恢复经济增长,但已经黔驴技穷。在国际清算银行货币基金组织的带领下,他们现在恳求各自的政府在利率很低的时候借更多的钱,希望更多的预算赤字能够阻止世界经济滑向衰退。

Other central banks are in the same boat

其它央行也处于同样的境地

The debt devil tempts,and the weak follow,and debtor hell is the highest reward he can offer.The response by all G20 members to a sliding global economy will obviously be a BIS sanctioned coordinated burst of deficit spending leading to a synchronised expansion of government bond supply and fiat money to pay for it.It is proving impossible,even for a free trader like Boris Johnson,to resist the political imperative to build new hospitals,train thousands of new nurses and policemen and throw money at a new,wildly over-budget railway connecting the North of England to London.Which,incidentally,will probably empty the North of northerners seeking their fortunes in London,instead of spreading London's wealth northwards.Most of this spending is classified as investment,but the fact is that without a commensurate increase in personal savings it is inflationary spending.

债务魔鬼诱惑,弱者跟随,债务人地狱是他能提供的最高报酬。面对全球经济的滑坡,G20所有成员国的反应显然将是国际清算银行批准的赤字开支的协调爆发,导致政府债券供应和为此支付的法定货币同步扩张。事实证明,即便是像鲍里斯•约翰逊(Boris Johnson)这样的自由贸易主义者,也不可能抵制政治上的迫切需求:建造新医院、培训数千名新护士和警察,以及向一条连接英格兰北部和伦敦的新建铁路投入大笔资金。顺便说一句,这可能会使北方人在伦敦寻找财富的人流失,而不是将伦敦的财富向北扩散。这些支出大部分被归类为投资,但事实是,如果个人储蓄没有相应增加,这就是通胀性支出。

Perhaps the dollar will not be the first to slide,given the shutting down of China's economy by the coronavirus.The yuan,surely,will be the first to suffer in the foreign exchanges,a process that appears to be starting.But this might galvanise the People's Bank into positive action to stabilise the currency,which it can do by tying it to gold.In doing so,it would do humanity a favour by leading the way early towards a sound money solution to the unfolding financial and economic crisis,which with the coronavirus threatens to be potentially much worse than anything recorded in modern times.

考虑到中国经济因这种冠状病毒而停滞不前,美元也许不会是第一个下跌的货币。毫无疑问,人民币将首先在外汇交易中受到冲击,这一过程似乎已经开始。但这可能会刺激中国央行采取积极行动,以稳定人民币汇率,央行可以通过将人民币与黄金挂钩来做到这一点。这样做,将为人类带来好处,带头为正在蔓延的金融和经济危机提供一个健全的货币解决方案,这场危机中的冠状病毒可能比现代记录中的任何危机都要糟糕得多。

The reason the dollar is likely to be next to slide is the exposure foreigners have to it,the equivalent of more than one year's GDP.It is comprised of about$4 trillion in bank deposits,and$19.4 trillion of US securities,according to the last available TIC figures.

美元之所以有可能继续下跌,是因为外国投资者对美元的风险敞口,相当于一年多的 GDP。根据互联网信息中心最新的数据,该基金包括约4万亿美元的银行存款和19.4万亿美元的美国证券。

For the short-term,perhaps China's imploding economy,taking Germany's and others with it,encourages the investor's myth that the dollar is a safe haven.The trade-weighted index has strengthened in recent weeks on the back of both the yuan and euro weakening,and US Treasury yields have declined as well.It is a situation unlikely to survive deteriorating economic conditions for much longer.

就短期而言,或许中国经济的内爆,连同德国和其它国家的经济一起,鼓励了投资者认为美元是安全避风港的神话。在人民币和欧元走软的推动下,贸易加权指数在最近几周有所走强,美国国债收益率也有所下降。这种情况不太可能在日益恶化的经济状况下持续很长时间。

In addition to foreign sellers,speculative positions of perhaps several trillion dollars in currency swaps held by large hedge funds will have to be reversed if and when the dollar is undermined by foreign selling.That would lead to temporary buying of euros and yen.When that short-term effect is over,presumably these currencies will then suffer the combination of collapsing values for government bonds and stockmarket values at the same time as the currencies themselves fall measured against gold,silver and bitcoin.

除了外国卖家,如果美元受到外国抛售的影响,大型对冲基金持有的可能数万亿美元货币互换的投机头寸将不得不逆转。这将导致欧元和日元的短期买盘。当这种短期效应结束后,这些货币可能会遭受政府债券和股市价值暴跌的双重打击,与此同时,相对于黄金、白银和比特币而言,这些货币本身也会下跌。

Sound money alternatives signal the fiat crisis

健全的货币替代品预示着不可兑现的危机

An unfolding crisis from the combined effects of the turn of the credit cycle and the coronavirus can be expected to hit individual fiat currencies both sequentially and generally.This article has made some suggestions over a likely sequence:yuan,dollar,euro and yen.But how things actually unfold is for the moment a matter of speculation.From the turmoil ahead of us,the clear winners are likely to be gold and silver,and supply-constrained hedges such as bitcoin.

信贷周期转变和冠状病毒的综合效应所导致的正在演变中的危机,可以预期将对个别法定货币产生连续而普遍的冲击。本文就人民币、美元、欧元和日元的可能走势提出了一些建议。但事情究竟如何发展目前还只是一个猜测的问题。从我们面前的动荡来看,明显的赢家可能是黄金和白银,以及供应受限的对冲工具,比如比特币。

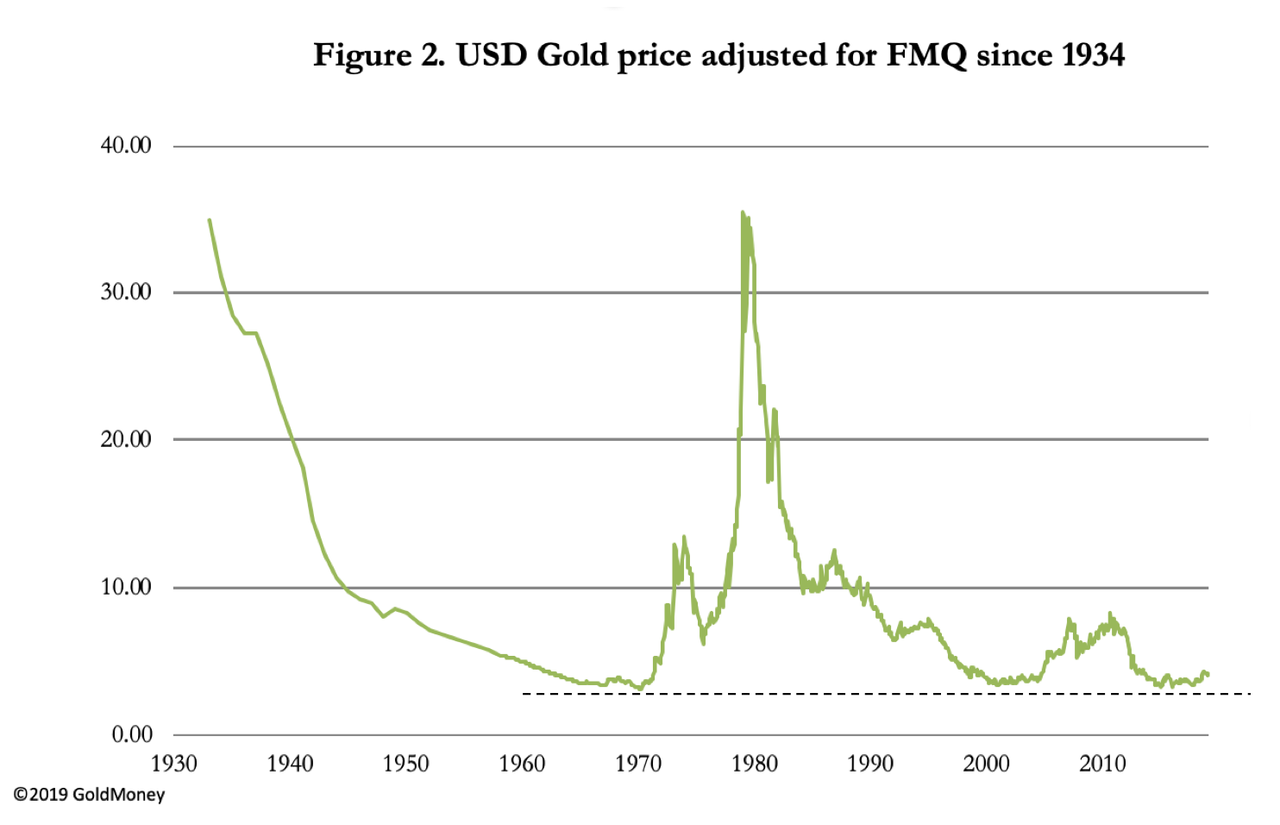

In real terms,gold is still under-priced relative to the dollar,based on their relative quantities.This is illustrated in Figure 2,which is of gold adjusted by the increase in the fiat money quantity.

按实际价值计算,根据黄金的相对数量,黄金相对于美元的价格仍然偏低。图2说明了这一点,它是黄金调整的法定货币数量的增加。

This chart should contradict any thoughts that the recent increase in the price of gold might be overdone.The truth is that the devastating bear market in the gold price following the spike in 1980 has almost eliminated gold from investment portfolios in favour of inflation beneficiaries.If that long period is coming to an end,investors will attempt to switch their allocations from inflation beneficiaries and bonds with rising yields in favour of inflation protection.For this reason,the rise in the dollar gold price could be very dramatic,particularly when a further acceleration of global monetary debasement is taken into account.And this is before we see official CPI measures move much above their 2%goal-sought targets.

这张图表应该与任何认为最近黄金价格上涨可能有些过头的想法相矛盾。事实是,在1980年黄金价格飙升之后,黄金价格出现了毁灭性的熊市,这几乎使黄金从投资组合中消失,而有利于通胀受益者。如果这段漫长的时期即将结束,投资者将试图将资产配置从通胀受益者和收益率不断上升的债券转向通胀保护。由于这个原因,美元黄金价格的上涨可能非常剧烈,尤其是考虑到全球货币贬值的进一步加速。而这还是在我们看到官方的 CPI 指标远远超过他们设定的2%目标之前。

For both gold and silver,we can expect initial moves reflecting their eventual replacement of failing fiat as the trusted money in circulation.In the case of silver,it is worth mentioning that its original price relationship under bimetallic standards only become discarded when silver was generally dropped as money in favour of gold alone in the 1870s.When fiat fails,it is likely that silver will regain a secondary monetary role,and its remonetisation will have a substantial impact on its purchasing power.From a current gold/silver ratio of 87 times,a move towards the old ratio of approximately 15 times means that for speculators buying into the sound money argument,silver is likely to be the catch-up form of sound money.

对于黄金和白银来说,我们可以预期,最初的举措反映出它们最终将取代失败的法定货币,成为流通中值得信赖的货币。就白银而言,值得一提的是,在19世纪70年代,当白银通常作为货币而仅以黄金为主时,它在双金属标准下的原始价格关系才被抛弃。当法定货币失败时,白银很可能重新获得次要货币角色,其再货币化将对其购买力产生重大影响。目前的黄金/白银比率为87倍,向旧比率约15倍的趋势意味着,对于买入稳健货币论的投机者而言,白银很可能是稳健货币的追赶形式。

Bitcoin

比特币

During previous currency hiatuses,the problem of failing fiat money has always been evidenced in the rising prices of precious metals.Since the last financial crisis,there has arisen a new category of store of value in thousands of different cryptocurrencies.While most of them appear to be akin to quack monetary remedies,the first cryptocurrency to be devised with its innovative blockchain technology is sufficiently understood by a growing band of followers to be firmly established as a form of money.

在以前的货币贬值期间,不兑现法定货币的问题一直体现在贵金属价格的上涨上。自上次金融危机以来,成千上万种不同的隐形货币出现了一种新的价值储存方式。虽然其中大多数似乎类似于江湖郎中的货币补救措施,第一个加密货币被设计与其创新的区块链技术是充分理解的追随者越来越多,被牢固确立为一种形式的货币。

Bitcoin is currently not ideally suited as a means of settling transactions,or for making value comparisons between one good against another.Settlements are severely restricted relative to the superior scalability offered by credit and debit cards.Where bitcoin scores is as a store of value.

目前,比特币并不是理想的交易结算工具,也不是进行商品价值比较的工具。相对于信用卡和借记卡所提供的高级可扩展性,结算受到严格限制。比特币的得分是一种价值储存。

In learning about bitcoin and why it works,a new generation of tech-savvy millennials have become aware of the way their governments debauch their currencies as a means of secretly transferring wealth from them as individuals to the state,the banks,and their favoured borrowers.Bitcoin supporters are an intelligent,educated mob angry at their governments'abuse of their fiat currencies.

在了解比特币及其运作原理的过程中,新一代精通技术的千禧一代已经意识到,他们的政府为了将个人财富秘密转移到国家、银行和他们偏爱的借款人手中,而贬低本国货币的方式。比特币支持者是一群受过教育的聪明暴徒,他们对政府滥用比特币感到愤怒。

In all populations,there is therefore a marginally greater recognition of the fragility of state currencies,and therefore the abandonment of them by the general public is likely to develop over a shorter time period than experience of previous instances would suggest.

因此,在所有人口中,对国家货币脆弱性的认识都略有提高,因此,公众放弃国家货币的时间可能比以往情况所显示的更短。

Conclusion

总结

The straws in the wind listed in this article point to a more rapid collapse of financial asset values and currencies than generally thought by sound money theorists who have long anticipated this outcome.Doubts about the timing have been settled to a degree by the sudden development of the coronavirus,which has already imploded China's economy,disrupting global supply chains and the provision of consumer goods.

本文中所列举的迹象表明,金融资产价值和货币的崩溃速度比健全货币理论家长期预期的结果更快。这种冠状病毒的突然发展,在一定程度上解决了外界对这一时机的疑虑。这种病毒已经使中国经济崩溃,扰乱了全球供应链和消费品供应。

To the extent the coronavirus has had a hand in the forthcoming destruction of fiat currencies and Keynesian mythology,we can take some comfort that it will have brought forward the eventual reintroduction of gold and gold standards.The path is not straightforward.There will be destruction of financial asset values and the economic consequences for ordinary people will be dire.We can expect widespread civil unrest and political instability.

在某种程度上,冠状病毒参与了即将到来的法定货币和凯恩斯主义神话的毁灭,我们可以感到一些安慰,因为它将带来最终重新引入黄金和黄金标准。这条道路并非一帆风顺。金融资产价值将遭到破坏,对普通民众的经济影响将是可怕的。我们可以预见到大范围的内乱和政治不稳定。

Western governments and their advisers are not familiar with the arguments in favour of gold,having spent half a century dismissing it.This fact favours the new economies which have not discarded gold,which include Russia,China,and many other Asian nations.Some governments,such as India,might attempt to confiscate their citizens'gold,but in general the collapse of western economic fallacies could lead to Asia's economic superiority.

西方政府及其顾问对支持黄金的论据并不熟悉,他们花了半个世纪的时间对黄金置之不理。这一事实有利于尚未抛弃黄金的新兴经济体,包括俄罗斯、中国和许多其它亚洲国家。印度等一些国家的政府可能会试图没收本国公民的黄金,但总体而言,西方经济谬论的崩溃可能会导致亚洲的经济优势。

It will be a rough ride for the rest of us.

对我们其他人来说,这将是一段艰难的旅程。

来源:https://www.zerohedge.com/geopolitical/will-covid-19-lead-gold-standard