04/25/2020

This article asserts that infinite money-printing is set to destroy fiat currencies far quicker than might be generally thought.This final act of monetary destruction follows a 98%loss of purchasing power for dollars since the London gold pool failed.And now the Fed and other major central banks are committing to an accelerated,infinite monetary debasement to underwrite their entire private sectors and their governments'spending,to prop up bond markets and therefore all financial asset prices.

这篇文章断言,无限制的印钞行为将以远比人们通常认为的更快的速度摧毁法定货币。自伦敦黄金储备失败以来,美元购买力下降了98%,随后出现了这种最后的货币破坏行为。现在,美联储和其他主要的中央银行正致力于加速、无限的货币贬值,以支持他们的整个私营部门和政府支出,支撑债券市场,从而支撑所有金融资产价格。

It repeats the mistakes of John Law in France three hundred years ago almost to the letter,but this time on a global scale.History,economic theory and even common sense tell us governments and their central banks will rapidly destroy their currencies.So that we can see how to protect ourselves from this monetary madness,we dig into history for guidance to see who benefited from the Austrian and German hyperinflations of 1922-23,and how fortunes were made and lost.

它几乎完全重复了三百年前约翰·劳在法国所犯的错误,但这一次是在全球范围内。历史、经济理论,甚至常识都告诉我们,各国政府及其央行将迅速摧毁本国货币。为了让我们看到如何保护自己免受这种货币狂热的影响,我们深入研究历史,看看谁从1922年至1923年奥地利和德国的超级通货膨胀中受益,以及财富是如何创造和流失的。

Introduction

引言

The way inflation is commonly presented by modern economists,as a rise in the general level of prices,is incorrect.The classical,pre-Keynesian definition is that inflation is an increase in the quantity of money which can be expected to be reflected in higher prices.For consistency and to understand the theory of money and credit we must adhere strictly to the proper definition.The effect on prices is one of a number of consequences,and is not inflation.

现代经济学家通常将通货膨胀描述为物价总水平的上升,这种方式是不正确的。经典的,前凯恩斯主义的定义是,通货膨胀是货币数量的增加,可以预期反映在更高的价格。为了一致性和理解货币信用理论,我们必须严格坚持正确的定义。对价格的影响是一系列后果之一,而不是通货膨胀。

The effect of an increase in the quantity of money and credit in circulation on prices is dependent on the aggregate human response.In a nation of savers,an increase in the money quantity is likely to add to savers'bank balances instead of it all being spent,in which case the route to circulation favours lending for the purpose of industrial investment.Product innovation,more efficient production and competitive prices result;and a price countertrend is introduced,whereby many prices will tend to fall,despite the increase in the money-quantity.

流通中货币和信贷数量的增加对价格的影响取决于人类的总体反应。在一个由储户组成的国家,货币数量的增加可能会增加储户的银行存款余额,而不是全部用于支出,在这种情况下,流通途径有利于为工业投资目的提供贷款。产品创新,更有效率的生产和具有竞争力的价格,并引入了价格反趋势,即许多价格将趋于下降,尽管增加货币数量。

We see this effect in electronic and other goods emanating from savings-driven economies in East Asia,notably Japan and China.But in economies where savings have been discouraged,particularly in America and the UK,there is less investment in production and a greater emphasis on imported goods.Immediate consumption dominates,and increased quantities of money in consumers'hands inevitably lead to a rise in the general price level of commonly demanded consumer goods.

我们在东亚储蓄驱动型经济体(尤其是日本和中国)的电子产品和其它商品中看到了这种效应。但在储蓄受到抑制的经济体中,尤其是在美国和英国,生产投资减少,更加重视进口商品。直接消费占主导地位,消费者手中货币数量的增加不可避免地导致普遍需求的消费品的总体价格水平上升。

In a world-wide fiat currency collapse,different savings characteristics between nations can be expected to lead to variations in the speed and timing of the decline of purchasing power between different currencies.We address this point later in this article and the consequences thereof.But a more immediate difficulty for observers is the habit of unquestionably accepting government measures of the general level of prices and incorrectly calling it inflation.

在全球法定货币崩溃的情况下,各国之间不同的储蓄特点可能会导致不同货币之间购买力下降的速度和时间的差异。我们将在本文后面讨论这一点及其后果。但观察人士面临的一个更直接的困难是,他们习惯于毫无疑问地接受政府的价格总水平衡量标准,并错误地将其称为通胀。

Don't trust government inflation statistics

不要相信政府的通货膨胀统计数据

The general level of prices is one of those economic concepts that cannot be measured.The policy of targeting a general level of prices through broad-based indices such as the CPI is thereby fatally flawed.The fundamental and incorrect assumption behind the concept of a consumer price index is that future demand does not vary from the historic,in other words the economy evenly rotates,and economic progress is banished from our thoughts.

价格的总体水平是无法衡量的经济概念之一。因此,通过消费物价指数等基础广泛的指数确定总体价格水平的政策存在致命缺陷。消费者价格指数概念背后的基本且不正确的假设是,未来的需求与历史没有任何变化,换句话说,经济均匀地转动,经济进步从我们的思想中消失了。

Furthermore,the broader the index,the more that extraneous factors,such as import substitution undermines the statistical concept of indexing domestic consumer prices.Together with the state's desire to reduce the apparent rate by using methods such as hedonics and product substitution,it explains why a CPI can rise at an average annual rate of just under 2%seemingly in perpetuity,while a more targeted index that focuses on everyday items,such as the Chapwood index comprised of 500 constant items,has returned an approximate 10%annual rate of price inflation for a number of years.And if you remove the distortions introduced by government statisticians over the last forty years as demonstrated by Shadowstats,you get a similar 10%approximation.

此外,指数范围越广,进口替代等外部因素就越损害指数化国内消费价格的统计概念。再加上政府希望通过享乐主义和产品替代等方法降低表面通胀率,这就解释了为什么 CPI 似乎可以永久性地以略低于2%的年均增长率增长,而一个更有针对性的、以日常用品为重点的指数,如由500个固定项目组成的 Chapwood 指数,多年来已经回报了大约10%的年通胀率。如果你去掉政府统计人员在过去四十年中引入的由 Shadowstats 所证明的扭曲,你会得到一个类似的10%的近似值。

What matters more than statistics is the effect on ordinary people.In their lack of knowledge about the consequences of changes in the quantities of money and bank credit,by default they see money as a constant,an objective factor in their transactions,with all the price changes emanating from the goods and services being bought or sold.They put rising prices down to profiteering,and when they fall,particularly for goods where product innovation is a strong influence,it is either explained by cheap foreign labour or just taken for granted.There is no public understanding of how inflation undermines the money side in transactions,nor,for that matter,how inflation transfers real savings and earning power from the individual to the state,which is the unstated objective of modern monetary policies.

比统计数字更重要的是对普通人的影响。由于他们对货币和银行信贷数量变化的后果缺乏了解,他们默认把货币看作是交易中的一个常量,一个客观因素,因为货币和服务的所有价格变化都来自于买卖。他们把价格上涨归咎于牟取暴利,而当价格下跌时,尤其是对于产品创新具有强大影响力的商品而言,要么是因为廉价的外国劳动力,要么就是理所当然。公众不了解通货膨胀如何在交易中损害货币方面,也不了解通货膨胀如何将实际储蓄和盈利能力从个人转移到国家,而这正是现代货币政策未明确阐述的目标。

It is ignorance of the role of money in this regard that permits governments to finance a significant and growing portion of their spending without resorting to unpopular taxation.Government debt issuance,which masquerades as a promise to repay the money borrowed,is mostly inflationary,sourced through monetary and bank credit expansion,that is when savers do not increase their savings.And in the desire to promote current consumption,American and British nationals in particular have been encouraged to spend all their income on consumer goods instead of adding to their savings.

正是由于对金钱在这方面的作用的无知,才使得政府能够在不征收不受欢迎的税收的情况下为其支出中越来越大的一部分提供资金。政府债务的发行冒充偿还借款的承诺,主要是通过货币和银行信贷扩张引起的通货膨胀,也就是说储户不增加储蓄。为了促进当前的消费,政府特别鼓励美国人和英国人把所有收入都花在消费品上,而不是增加储蓄。

The recycling of capital from trade deficits into government and other securities is inflationary as well.When foreign businesses in the import trade or their governments buy a state's government debt,the origin of their currency purchased can almost always be traced back to domestic credit expansion.American trade deficits since 1992,having accumulated to$12 trillion matches foreign ownership of the sum of US Treasuries,asset-backed securities and short-term debt almost precisely.

将资本从贸易逆差转化为政府和其它证券也会导致通胀。当从事进口贸易的外国企业或其政府购买一国政府债务时,购买其货币的来源几乎总是可以追溯到国内信贷扩张。自1992年以来,美国贸易赤字累计达到12万亿美元,与外国持有的美国国债、资产支持证券和短期债务的总和几乎完全一致。

Given proclamations by central bankers that they are about to hyperinflate,ignorance of monetary matters becomes an expensive condition.When trying to understand money,credit and how they flow,the vast majority of people find themselves in an Alice in Wonderland confusion where nothing makes sense.They are setting themselves up to lose everything they possess.

鉴于各国央行行长宣称他们即将实施过度通货膨胀,对货币问题的无知将成为一种代价高昂的状况。当人们试图理解金钱、信用以及它们是如何流动的时候,绝大多数人都会发现自己处于一种爱丽丝梦游仙境混乱之中,一切都毫无意义。他们把自己置于失去一切的境地。

The first phase of inflation is ending

通货膨胀的第一阶段即将结束

For most people the persuasive argument is empirical evidence,assuming they are prepared to look for it.We all understand that over time,our dollars,pounds and euros buy less.But despite the evidence,almost no one is really aware of the extent their fiat currencies have declined.

对于大多数人来说,如果他们准备好去寻找,那么说服性的论据就是经验证明。我们都明白,随着时间的推移,我们的美元、英镑和欧元买得越来越少。但是,尽管有这些证据,几乎没有人真正意识到它们的法定货币贬值的程度。

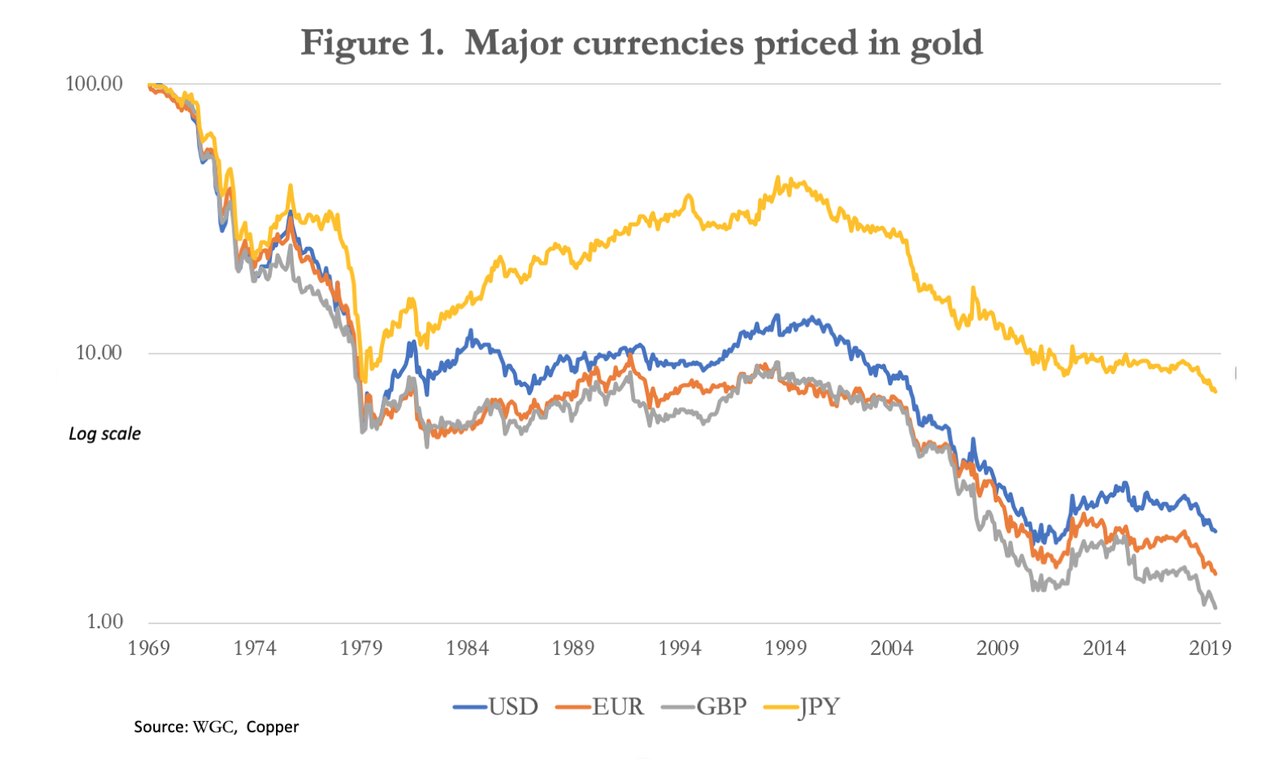

I make no apologies for having used the chart in Figure 1 before,but it is necessary to ram the point home.Since the dollar was devalued from$35 in the late 1960s,measured against gold the dollar has retained only 2.2%of its 1969 purchasing power.Admittedly,one would expect gold's purchasing power to gently rise over time,which has been the experience under gold standards,exaggerating the dollar's decline.

对于之前使用了图1中的图表,我并不感到抱歉,但是有必要将这一点用 ram 代替。自从美元从上世纪60年代末的35美元贬值以来,美元对黄金的汇率仅保持了其1969年购买力的2.2%。不可否认,人们会预计黄金的购买力会随着时间的推移逐渐上升,这是金本位制下的经验,夸大了美元的下跌。

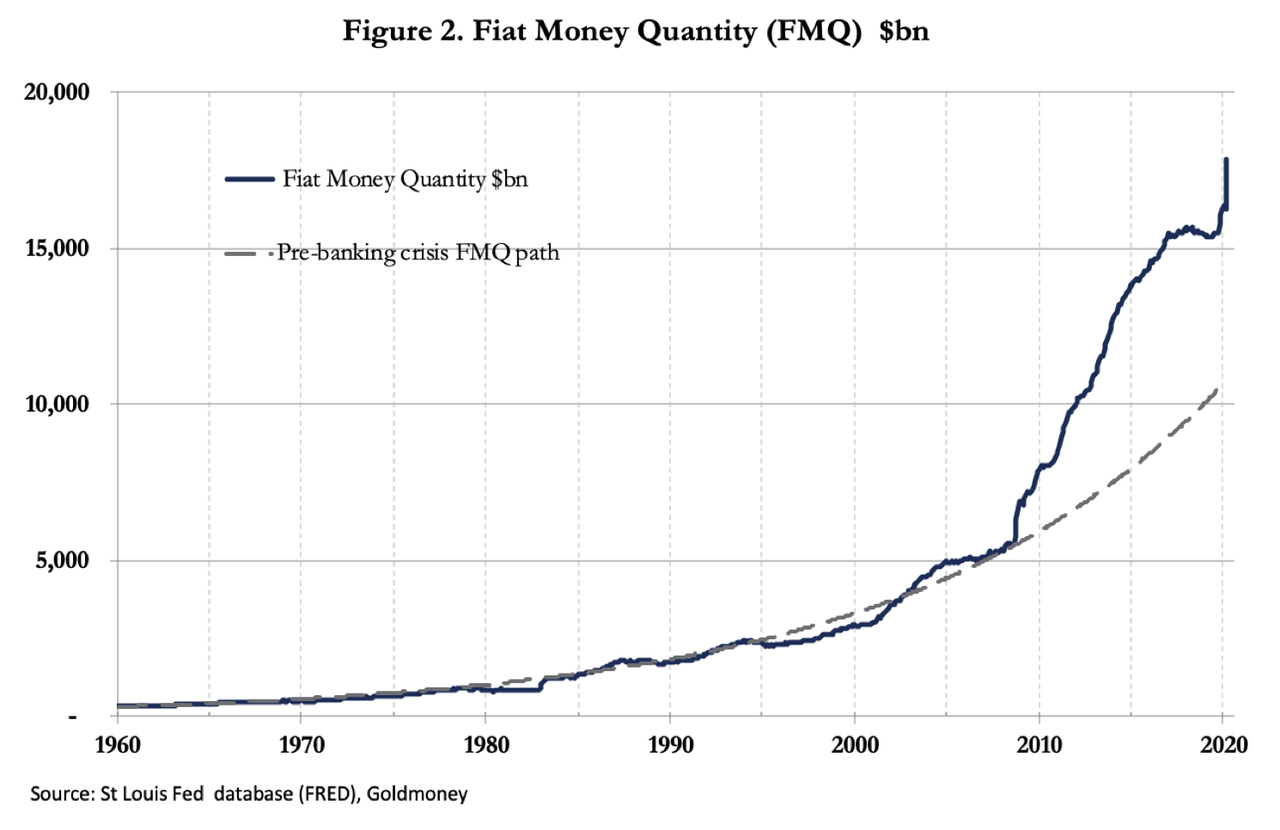

But critics of the approach of measuring fiat currencies against gold should note that measured by broad money(M3)only 3.8%of the dollar's 1969 purchasing power remains,and when the increase in bank reserves not in circulation is taken into account,the figure falls to 3.2%,much closer to that indicated by comparison with gold.The inclusion of bank reserves,reflected in the fiat money quantity,is illustrated in Figure 2,and shows that the increase in the money quantity has recently become vertical.

但是,对于用黄金来衡量法定货币的方法持批评态度的人士应该注意到,以广义货币(M3)来衡量,美元1969年的购买力只有3.8%。如果把非流通中的银行储备的增加计算在内,这个数字下降到了3.2%,与黄金相比更接近。包括银行储备,反映在法定货币数量,是在图2中说明,并显示货币数量的增加最近已成为垂直。

The rapid monetary expansion before 1 March(the most recent available underlying statistics),was before the US lockdown and has continued since.So far,this has been only Phase 1 of the decline of fiat currencies,the warm-up act for a total currency collapse,which we will call Phase 2.It is increasingly certain with every passing day that we are now embarking on that second phase,which is now the focus of this article.

3月1日之前的快速货币扩张(可获得的最新基本统计数据)发生在美国封锁之前,此后一直持续。到目前为止,这只是法定货币衰退的第一阶段,是货币全面崩溃的预热阶段,我们称之为第二阶段。随着时间的推移,我们越来越确信,我们现在正在进入第二阶段,这也是本文的重点。

The second phase–currency destruction

第二阶段——货币毁灭

With the general public and virtually all the financial establishment ignorant of or blind to the inflationary situation,central banks have chosen this moment to announce unlimited monetary expansion to buy off the consequences of the coronavirus.They have committed to the virtual nationalisation of their economies,to be paid for by debauching their currencies.The process depends on public ignorance of the consequences.In all the announcements of government support for their economies and of their central banks'monetary role,there has been virtually nothing said or written about the consequences of the monetary inflation involved.

由于普通民众和几乎所有的金融机构对通胀情况一无所知或视而不见,各国央行选择此时宣布无限制的货币扩张,以收买冠状病毒的后果。他们已经承诺对他们的经济进行实质上的国有化,通过借记他们的货币来支付。这个过程取决于公众对后果的无知。在所有政府宣布支持本国经济和央行货币角色的声明中,几乎没有任何关于货币通胀后果的言论或文章。

Indeed,the only thing more astounding than the ignorance of the general public over monetary matters is the apparent ignorance of the politicians and central bankers charged with implementing monetary policy.But the brakes are now off,the chasm beckons,and the purchasing powers of fiat currencies are set to run downhill at a rapidly accelerating pace.We are now about to embark on Phase 2,when it dawns on the public that with respect to prices money is collapsing and will soon become worthless.

事实上,比公众对货币问题的无知更令人震惊的是,负责执行货币政策的政治家和央行行长们显然对此一无所知。但现在刹车已经关闭,鸿沟在召唤,法定货币的购买力将以迅速加速的步伐走下坡路。我们现在即将开始第二阶段,这时公众开始意识到,就价格而言,货币正在崩溃,不久将变得一文不值。

The process of a developing collapse of a fiat currency usually starts with foreigners reducing their exposure to it.In the case of Austria and Germany in 1922-1923,foreigners sold the crown and the paper mark respectively for dollars freely convertible into gold.In John Law's day,it was astute speculators who could sense a failing project and whose selling of his Mississippi venture and Law's unbacked livres for foreign currencies and specie overwhelmed Law's plans.Today,both cross-border strategic positions and portfolio investment are stalling and threatening to reverse.Ahead of the event it is impossible to judge their sequencing;but the dollar having the role of reserve currency appears to be most exposed to foreign liquidation,with foreigners holding equities,boned,deposits and cash totalling some$25 trillion,significantly more than America's GDP.

法定货币发展崩溃的过程通常始于外国人减少他们对法定货币的敞口。在1922年至1923年间的奥地利和德国,外国人分别出售皇冠和纸币,换取可自由兑换成黄金的美元。在约翰·劳的时代,精明的投机者能够察觉到一个失败的项目,并且他出售密西西比州的冒险和劳的无担保利弗换取外汇和硬币的计划压倒了劳。如今,跨境战略头寸和证券投资都陷入停滞,并有可能出现逆转。在事件发生之前,不可能判断他们的顺序;但是美元作为储备货币的角色似乎最容易受到外国清算的影响,外国人持有的股票、骨架、存款和现金总计约25万亿美元,远远超过美国的国内生产总值。

To address their escalating liabilities at home,foreign governments and businesses will require financial resources currently invested in US securities to be repatriated.Foreign central banks have their own economies to rescue.Businesses everywhere are suddenly facing mounting losses and have no alternative but to reduce their dollar exposure.Foreign portfolio managers are being spooked by a developing worldwide bear market and seem certain to liquidate their US holdings and their dollar positions in the coming months.

为了应对国内不断增长的债务,外国政府和企业将需要将目前投资于美国证券的财政资源汇回国内。外国央行也有自己的经济需要拯救。世界各地的企业突然面临越来越大的损失,别无选择,只能减少美元风险敞口。全球熊市的发展令外国投资组合经理惊慌失措,他们似乎肯定会在未来几个月清算所持美国资产和美元头寸。

Diminishing cross-border trade and the shock of the coronavirus have fundamentally undermined demand for dollars.This is not to be confused with demand for dollar liquidity,which some say will support the dollar.Liquidity is required in all currencies,which will be satisfied by liquidation of financial assets.The ensuing collapse of financial asset values and foreign liquidation of dollars is increasingly likely because all classes of foreign investors have,until now,enjoyed the security of investing in the world's reserve currency,while Americans have generally avoided owning foreign currencies.It is only a matter of time before this imbalance begins to undermine the dollar,and then consequences will follow.

跨境贸易的减少和冠状病毒的冲击已从根本上削弱了对美元的需求。这不应与对美元流动性的需求相混淆,一些人表示,这种需求将支撑美元。所有货币都要求有流动性,这些流动性将通过清算金融资产得到满足。随之而来的金融资产价值暴跌和外国对美元进行清算的可能性越来越大,因为迄今为止,所有类别的外国投资者都享有投资于全球储备货币的安全感,而美国人一般都避免持有外汇。这种不平衡开始破坏美元只是个时间问题,然后后果就会随之而来。

The dollar problem has arisen partly because interest rates are too low.The comparison is not to be made against negative rates in other currencies,but in the context of the domestic US economy.From rising food prices,deteriorating government finances and falling stock prices,other factors will flow.Bond yields,which cannot fall by much,will begin to rise as the government deficit increases,particularly with foreign buyers for US Treasuries being absent.Inevitably,the Fed will then come under pressure from markets to raise interest rates.In the face of an economic slump this will be resisted,and the exchange rate will fall.As the banker of last resort for the US government,the deteriorating economy,and for the rest of the world,the Fed will not only be financing everything but forced into buying bonds the foreigners and others sell as well.

美元问题之所以出现,部分原因在于利率过低。这种比较不是针对其它货币的负汇率,而是针对美国国内经济进行的。从上涨的食品价格,恶化的政府财政和下跌的股票价格,其他因素将流动。随着政府赤字增加,债券收益率(不会大幅下降)将开始上升,尤其是在外国买家缺席的情况下。届时,美联储将不可避免地面临来自市场的加息压力。面对经济衰退,这种做法将受到抵制,汇率也将下跌。作为美国政府、日益恶化的经济以及全球其它地区的最后一根救命稻草,美联储不仅将为一切融资,还将被迫购买外国人及其它投资者出售的债券。

On both Wall Street and Main Street,Americans are bound to become increasingly aware of the inflationary consequences.The problem for the Fed is that there is no Plan B alternative to financing by means of inflation of money and credit,particularly in an election year.

在华尔街和普通民众中,美国人注定会越来越意识到通货膨胀的后果。美联储面临的问题是,除了通过货币和信贷的通货膨胀进行融资,没有其他备选方案,尤其是在选举年。

After a persistent and unusually protracted period of monetary inflation over the last fifty years,it is increasingly likely the public will finally understand what is happening to prices.They will then begin to realise that it is excessive quantities of money in circulation that is the reason for rising prices,and that they must dispose of currency as quickly as possible for anything they want or can barter in future for something else.Empirical evidence is that this second and final phase of monetary debasement is likely to last only a matter of months.

在经历了过去50年持续的、不寻常的长期货币通货膨胀之后,公众越来越有可能最终理解价格正在发生什么。然后,他们会开始意识到,正是流通中的货币数量过多才导致物价上涨,他们必须尽快抛售货币,以换取他们想要的任何东西,或者将来可以用货币来换取其他东西。经验证明是货币贬值的第二阶段也是最后阶段可能只会持续几个月。

Once this second phase starts,it is almost impossible to stop it,because the public will have lost faith not just in the currency,but in the government establishment's monetary and economic policies as well.It ends when an unbacked fiat currency is no longer accepted as money by the public.

一旦第二阶段开始,几乎不可能阻止它,因为公众不仅会对货币失去信心,还会对政府机构的货币和经济政策失去信心。当一种没有支持的法定货币不再被公众接受为货币时,它就结束了。

Currency dysphasia

货币吞吐困难

In the past,an inflationary collapse has usually affected currencies in isolation;but the modern tendency for governments to coordinate their inflationary stimulations raises a new factor,of strains between currencies collapsing at the same time but at different rates.

在过去,通货膨胀的崩溃通常孤立地影响货币;但现代政府协调其通货膨胀刺激的趋势提出了一个新的因素,货币之间的紧张在同一时间崩溃,但在不同的速度。

The most notable experience of it in modern times was in several European countries following the First World war.The inflations were individual to the nations,but the cause was the same,and Austria's inflationary collapse ran ahead of Germany's.A passage from a man who witnessed it,the Austrian writer Stefan Zweig,in his autobiographical The World of Yesterday vividly describes the consequences:

近代最值得注意的经验是在第一次世界大战之后的几个欧洲国家。通货膨胀对于各个国家来说是个别的,但原因是一样的,奥地利的通货膨胀崩溃比德国的要早。奥地利作家斯特凡•茨威格(Stefan Zweig)在他的自传体小说《昨日的世界》(The World of Yesterday)中,有一段话生动地描述了这一切的后果:

Every hotel in Vienna was filled with these vultures[foreign tourists];they bought everything from toothbrushes to landed estates,they mopped up private collections and antique shop stocks before their owners,in their distress,woke to how they were being plundered.Humble hotel clerks from Switzerland,stenographers from Holland would put up in the deluxe suites of the Ringstrasse hotels.Incredible as it may seem,I can vouch for it as an eyewitness that Salzburg's first-rate Hotel de l'Europe was occupied for a period by English unemployed,who,because of Britain's generous dole were able to live more cheaply at that distinguished hostelry than in their slums at home.Whatever was not nailed down disappeared.The tidings of cheap living and cheap goods in Austria spread far and wide;greedy visitors came from Sweden from France;more Italian French Turkish and Romanian was spoken than German in Vienna's business district.

维也纳的每家旅馆都挤满了这些贪婪的(外国游客);他们购买从牙刷到地产的一切东西,他们清理私人收藏品和古董店的库存,直到他们的主人痛苦地意识到他们是如何被掠夺的。来自瑞士的不起眼的酒店职员,来自荷兰的速记员会在 Ringstrasse 酒店的豪华套房里安顿下来。尽管这看起来难以置信,但作为一个目击者,我可以担保,萨尔茨堡一流的欧洲旅馆曾一度被英国失业者占据,由于英国慷慨的救济金,他们能够住在那家著名的旅馆里,而不是住在家里的贫民窟里。任何没有钉牢的东西都消失了。在奥地利,廉价生活和廉价商品的消息广为流传;贪婪的游客来自法国的瑞典;在维也纳的商业区,更多的人说意大利语、法语、土耳其语和罗马尼亚语,而不是德语。

Among the Austrians impoverished in their own communities,the law-abiding starved and those prepared to break food rationing laws thrived.Savers,who had patriotically bought government bonds,lost everything.Germans from across the border,whose currency was yet to enter its final collapse,could swill six litres of Austrian beer for one of German,adding to the foreign revelry in Austria's misery.

在自己社区的奥地利穷人中,守法的饥饿者和准备违反食物配给法的人发展得很好。出于爱国心购买政府债券的储户们失去了一切。边境另一边的德国人,他们的货币还没有进入最后的崩溃,可能会为一个德国人喝掉6升的奥地利啤酒,加剧外国人对奥地利苦难的狂欢。

In our contemporary fiat collapse,differences in its rate will create similar openings for an unsettling life arbitrage.In business dealings,any vestiges of decency and compassion are early victims as those with an early understanding of the opportunities provided by a monetary collapse profit from the innocence of the ignorant.But Germany was to suffer the inflationary fate of Austria the following year.Again,from Zweig:

在我们当代的菲亚特崩溃,其速度的差异将创造一个令人不安的生活套利类似的开口。在商业交易中,任何正派和同情的痕迹都是早期的受害者,因为他们早就知道金融崩溃带来的机会,从无知者的天真中获利。但是第二年德国将遭受奥地利通货膨胀的命运。茨威格再次表示:

A pair of shoe laces cost more than a shoe had once cost,no,more than a fashionable store with two thousand pairs of shoes had cost before;to repair a broken window more than the whole house had formerly cost,a book more than the printers shop with a hundred presses.For$100 one could buy rows of six-storey houses on Kurfürstendamm and factories were to be had for the old equivalent of a wheelbarrow…

一双鞋带的价格曾经比一双鞋子的价格还要高----不,比一家时髦的商店以前卖两千双鞋子的价格还要高;修理一扇破窗子的价格比整个房子以前的价格还要高----修理一本书的价格比拥有一百台印刷机的打印店的价格还。花上100美元,你就可以在 Kurfürstendamm 买到一排排六层楼的房子,工厂也可以买到老式的手推车.....。

…Towering over all of them was the gigantic figure of the super-profiteer Stinnes expanding his credit and in thus exploiting the mark he bought whatever was for sale,coal mines and ships,factories and stocks,castles and country estates,actually for nothing because every payment,every promise became equal to naught.Soon a quarter of Germany was in his hands and,perversely,the masses who in Germany always became intoxicated at a success that they can see with their eyes,cheered him as a genius.

......超级牟利者斯廷内斯的巨大人物耸立在他们之上,他扩大自己的声誉,因此利用他买来的任何东西——煤矿和船只、工厂和股票、城堡和乡村庄园——来赚钱,实际上却是一无所获,因为每一笔付款,每一个承诺都等于零。很快,四分之一的德国就掌握在他的手中,而且,反常的是,德国的大众总是陶醉于他们亲眼所见的成功,为他的天才之作而欢呼。

The story of Hugo Stinnes brings us back to our current situation,how markets will evolve and who will profit.

雨果·斯廷内斯的故事把我们带回到当前的形势,市场将如何演变,谁将从中获利。

The fate of financial investments

金融投资的命运

All the intentions of providing business with credit,helicoptered money,replacing lost taxes and ensuring government is financed,can be pared down to a single policy objective:the support of financial asset values.If the markets fail,all else fails.

向企业提供信贷、直升机输送资金、弥补税收损失和确保政府融资的所有意图,都可以缩减为一个单一的政策目标:支持金融资产的价值。如果市场失灵,其它一切都将失败。

In today's fiat currency world,the principal asset from which all others take their valuation is government debt.But that has run out of road,with US Treasury debt yielding less than one per cent for all but the longest maturities,and in Europe,Switzerland and Japan unnatural negative rates are common.Foreign ownership of US Treasuries and other financial assets,which has long been the counterpart of trade deficits and portfolio inflows,is now greater than the US's GDP and will almost certainly become a source of funds for foreign governments,businesses and investment portfolios in difficulty themselves.

在当今的法定货币世界,所有其他货币的估值所依据的主要资产是政府债券。但这种情况已经走到了尽头,除最长期限外,美国国债的收益率都低于1%,而在欧洲、瑞士和日本,非自然的负利率很常见。长期以来,美国国债和其它金融资产一直是贸易赤字和投资组合流入的对应物。如今,外国对美国国债和其它金融资产的持有量超过了美国的国内生产总值(GDP),而且几乎肯定会成为陷入困境的外国政府、企业和。

Commercial banks are in a mood to contract their balance sheets,initially due to liquidity constraints and now increasingly driven by abject fear.With demand for new government debt thereby limited,the Fed,together with central banks in other jurisdictions,will find that they are effectively the only significant actors on the buy side for not just government debt,but a wider range of financial assets as well.

商业银行有意收缩自己的资产负债表,最初是由于流动性限制,现在则越来越受到可怜的担忧的驱使。由于对新政府债券的需求因此受到限制,美联储和其他地区的央行将发现,它们实际上不仅是政府债券买方的唯一重要参与者,而且是范围更广的金融资产买方。

The Fed has already stated it will offer additional support to bond markets by buying exchange traded funds invested in corporate bonds.By putting a floor under bond spreads,the Fed obviously hopes to support everything from junk to investment grade,because if it did not,spreads would blow out even more,threatening bank balance sheets which are thought to carry some$2 trillion of this debt both directly and in collateralised loan obligations.

美联储已经表示,将通过购买投资于企业债券的交易所交易基金(etf),为债券市场提供额外支持。通过为债券息差设定底线,美联储显然希望支持从垃圾级到投资级的所有债券,因为如果不这样做,息差将进一步扩大,威胁到银行的资产负债表,这些资产负债表被认为直接或以贷款抵押债券的形式背负着大约2万亿美元的债务。

The Fed already supports house prices by buying mortgage debt.It hopes that by preserving a wealth effect,investors will not only continue to feel well off but be encouraged to keep investing.The policy is to swamp financial markets with new money.The other side of the Fed buying financial assets of any description is the payment for them,expanding the quantity of money in circulation.

美联储已经通过购买抵押贷款债券来支撑房价。它希望通过保留财富效应,投资者不仅会继续感到富裕,而且会被鼓励继续投资。政策是用新钱淹没金融市场。美联储购买任何种类的金融资产的另一方面是为这些资产支付费用,从而扩大流通中的货币数量。

The overwhelming imperative to keep control of markets is a recipe for hyperinflation and will ultimately fail.The Fed would have us believe that the slump in business activity is only due to the coronavirus lockdown and that shortly after it ends normality will return.It will hope that we have forgotten that fully five months before the virus hit,it was forced to inject liquidity into the repo market at the rate of tens of billions every day.

保持对市场的控制势在必行,这是恶性通货膨胀的处方,最终会失败。美联储想让我们相信,商业活动的下滑仅仅是由于冠状病毒的封锁,并且在它结束后不久将恢复正常。它希望我们忘记,在病毒袭击前整整五个月,它被迫以每天数百亿美元的速度向回购市场注入流动性。

The Fed's monetary policy replicates John Law's attempt to keep his bubble going in 1720 France.Law failed to maintain the price of just one asset,the Company of the Indies,his Mississippi venture,by printing livres to buy the shares.Within seven months the currency had collapsed and priced in worthless currency,the shares had fallen from 12,000 livres to just one or two thousand.

美联储的货币政策重复了约翰·劳在1720年法国为保持泡沫所做的努力。通过印刷里弗斯来购买股票,劳未能维持他在密西西比州的风险投资——印度公司——这一资产的价格。在七个月内,货币崩溃,以毫无价值的货币计价,股价从12,000里弗跌到仅仅1,2000里弗。

The principal upon which the Fed and the other major central banks are embarked is the same in every respect,but with a far larger task.The project will fail for the same reason:no one can fool all of the people all of the time.It is increasingly obvious that both the currency and financial asset values will collapse John Law-style,probably by the end of this calendar year,if precedents are any guide.

美联储和其他主要中央银行所依据的原则在各个方面都是一样的,但是任务更加艰巨。这个项目会因为同样的原因而失败:没有人可以一直欺骗所有的人。越来越明显的是,货币和金融资产的价值都将崩溃,约翰·劳式的崩溃,可能在今年年底,如果先例可以作为指导的话。

There will be economic turmoil,with businesses and their banks collapsing,for which yet more quantities of money will be required to discharge the socialistic imperative.There will be a new currency,whether it is an attempted government reset which will only delay the ending of fiat currency for a few more months,or one that evolves from gold or silver and their credible substitutes.

随着企业及其银行的倒闭,经济动荡将会到来,为了履行社会主义的使命,还需要更多的资金。将会出现一种新的货币,无论是政府尝试重置法定货币,只会将法定货币的终结推迟几个月,还是从黄金或白银及其可靠的替代品演变而来。

Those seeking to profit from the situation will emulate the Inflation King,Hugo Stinnes,who bought real,instead of financial assets.As Zweig put it in the second extract quoted above,whatever was for sale,coal mines and ships,factories and stocks,castles and country estates,actually for nothing because every payment became equal to naught.But among financial assets,there could be shares of businesses that will survive,but stock markets being dependent on fiat money will be finished.Thinking that there is some protection from inflation in equities has been true in Phase 1 of the inflationary collapse,the last fifty years to date.But in Phase 2,a sudden global collapse of the fiat currency system,financial assets are probably to be avoided.

那些试图从中获利的人将效仿"通货膨胀之王"(Inflation King)雨果•斯廷内斯(Hugo Stinnes),他购买的是真实资产,而非金融资产。正如茨威格在上文引用的第二段话中所说,无论出售什么----煤矿和船只、工厂和股票、城堡和乡村庄园----实际上都是免费的,因为每一笔付款都等于零。但在金融资产中,可能会有企业的股票存活下来,但依赖法定货币的股票市场将会结束。在通胀崩溃的第一阶段,也就是过去50年到目前为止,认为股票可以抵御通货膨胀的想法是正确的。但在法定货币体系突然全球崩溃的第二阶段,金融资产可能是要避免的。

By far the best strategy is to have sound money at the outset.When$100 could buy rows of six-storey houses on Kurfürstendamm in Berlin and factories were to be had for the old equivalent of a wheelbarrow,the dollar was gold-backed.Today,with all currencies set to collapse there are no substitutes for gold itself,the only exception being silver.A case could be made for bitcoin,and other restricted-issue distributed ledger cryptocurrencies,but is yet to be proven.The adventurous will borrow fiat to buy bullion today,in the expectation the fiat repayment will cost them nothing.And what better opportunity is the gift presented to present day inflation kings than the suppression of interest rates by central bankers.

到目前为止,最好的策略是在一开始就拥有稳健的货币。当100美元可以在 Kurfürstendamm 买到一排排六层楼高的房子,工厂可以买到老式的手推车时,美元是黄金支持的。今天,随着所有货币的崩溃,没有任何东西可以替代黄金本身,唯一的例外是白银。比特币和其他受限制的分布式分类账加密货币可能会成为一个案例,但还有待证明。如今,敢于冒险的人会借钱购买黄金,因为他们预期,法定偿还不会让他们付出任何代价。还有什么比中央银行家抑制利率更好的机会是送给当今通胀之王的礼物呢。

来源: